The tone established late last week has carried into the new trading week, with risk appetite remaining firm despite a relatively quiet macro calendar. While scheduled event risk is lighter than in recent weeks, traders still face several catalysts, including the June FOMC minutes, the RBNZ policy decision, US ISM Services PMI, Canada's employment report and China's CPI inflation data.

Equity markets will also be closely watching SpaceX's inclusion in the NASDAQ 100, SK Hynix's ADR joining the index later in the week, and positioning for the start of the US Q2 earnings season.

Risk sentiment remains constructive

The platform established late last week has spilled into the new trading week and, with limited weekend news to materially impact pricing, the Asia open has so far been orderly. There have, however, been several notable developments beneath the surface.

NAS100 futures are trading around 1.4% higher after Hon Hai Precision reported quarterly sales growth of 40%, driven by continued strength in AI infrastructure demand. As one of Nvidia's key manufacturing partners, investors are interpreting the results as another constructive read-through for GPU demand and the broader semiconductor ecosystem.

Samsung has also reportedly increased DRAM prices by around 20% for customers. While this highlights the company's pricing power and continued strength in memory markets, it also reinforces the inflationary pressures emerging within the AI infrastructure build-out, potentially increasing costs across the semiconductor supply chain.

Gold briefly traded above $4,200 at the Asia open before giving back those gains, with futures liquidity remaining relatively thin, although this should build into the Shanghai futures markets open.

European equity futures will also come into focus. With formal cash market participation limited late last week, traders will be watching to see whether recent momentum extends into another session of European equity outperformance.

FX markets remain relatively subdued. USDJPY has attracted modest buying interest, although broader USD pairs remain mixed, and directional conviction is lacking. The US 2-year Treasury yield remains anchored near 4.13%, comfortably within its recent 4.06% to 4.20% range.

A lighter macro calendar, but still plenty to watch

Compared with recent weeks, scheduled event risk is lighter. Instead, the market's attention is likely to shift towards portfolio rotation, broader macro developments and positioning ahead of the US Q2 earnings season.

The US ISM Services PMI has the potential to move markets, but only if we see a meaningful surprise relative to consensus expectations of 54.0.

The June FOMC minutes should also attract attention after the volatility generated by the latest dot plot and Fed Chair Kevin Warsh's press conference. Prior to the US employment report, overnight index swaps implied around a 40% probability of a July Fed rate hike. Following stronger-than-expected payrolls, those expectations have fallen back towards 19% and could decline further should June CPI, due on 14 July, print softer than expected.

Canada's employment report and China's CPI inflation figures are also on the calendar. While neither is expected to materially alter the outlook for their respective central banks, so any significant surprise could see volatility contained.

RBNZ decision could inject volatility into the NZD

The RBNZ is expected to raise the OCR by 25 basis points. However, a hike is far from guaranteed, with NZD OIS currently pricing around 17.5 basis points of tightening, markets imply a 70% probability of a 25bp increase. Adding further uncertainty, the RBNZ Shadow Board has today recommended leaving rates unchanged.

As a result, both the policy decision and the accompanying guidance have the potential to generate meaningful volatility in the New Zealand dollar.

SpaceX joins the NASDAQ 100

Tuesday marks SpaceX's inclusion in the NASDAQ 100, with the primary buying associated with the rebalance should come from passive index funds and benchmark-tracking portfolios completing their purchases during Monday's closing auction.

While some expect index inclusion to act as a meaningful catalyst for the share price, historical evidence from recent IPO additions suggests these effects are often short-lived, and often failing to provide any meaningful impact at all...

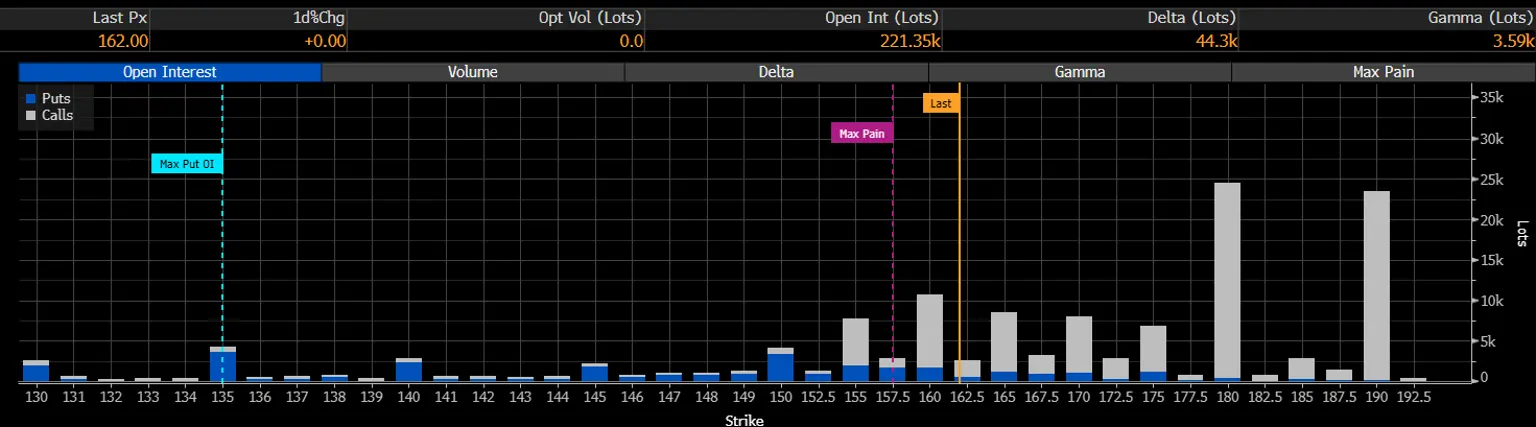

More interesting is the options market. Open interest across options expiring on 10 July is concentrated around the $180 and $190 call strikes. Should SpaceX continue to rally towards these levels, dealer hedging activity could amplify upside momentum and increase realised volatility.

Rather than expecting sustained buying from passive flows alone, traders may find greater opportunities in the higher volatility that index inclusion can create.

SK Hynix may attract even greater attention

While SpaceX is likely to dominate headlines early in the week, Friday's addition of SK Hynix's ADR to the NASDAQ 100 could prove equally, if not more, significant. Samsung's 20% increase in DRAM pricing reinforces the constructive backdrop for the memory industry, and investors will naturally question whether SK Hynix follows with similar pricing actions.

SK Hynix remains one of the world's highest-profile AI beneficiaries, with daily price action increasingly driven by positioning, leveraged ETF rebalancing and flow-based dynamics. The ADR's inclusion provides international investors with another highly liquid vehicle to express views on AI infrastructure demand and raises the question of whether capital rotates away from names such as Micron into SK Hynix.

US earnings season begins

Elsewhere, PepsiCo (not shown on the calendar) and Delta Air Lines unofficially begin the US Q2 earnings season.

While these reports are unlikely to dominate trading activity on their own, they establish the tone for the weeks ahead, with the major US banks beginning to report the following week and earnings season moving into full swing.

Bottom line

Although the macro calendar is lighter than traders have become accustomed to, there are still several important catalysts capable of driving volatility. Between the FOMC minutes, the RBNZ decision, SpaceX and SK Hynix joining the NASDAQ 100, and the beginning of the US Q2 earnings season, markets should continue to provide opportunities across equities, FX, rates and volatility throughout the week.

Good luck to all.