- English

- 中文版

Equity Rally Rolls On With Pain Trade Remaining Higher

Amid reports that a US-Iran MoU to end the ongoing conflict is close to being agreed, market optimism has been unleashed once more.

Risk Rally Takes Another Leg Higher

Stocks, predictably, have surged across the board, albeit with notable outperformance coming through in European markets, reflecting the continent’s greater exposure to the downside macro risks that the conflict has triggered, and the subsequent greater ‘sigh of relief’ that can be breathed on signs that light may be at the end of the tunnel.

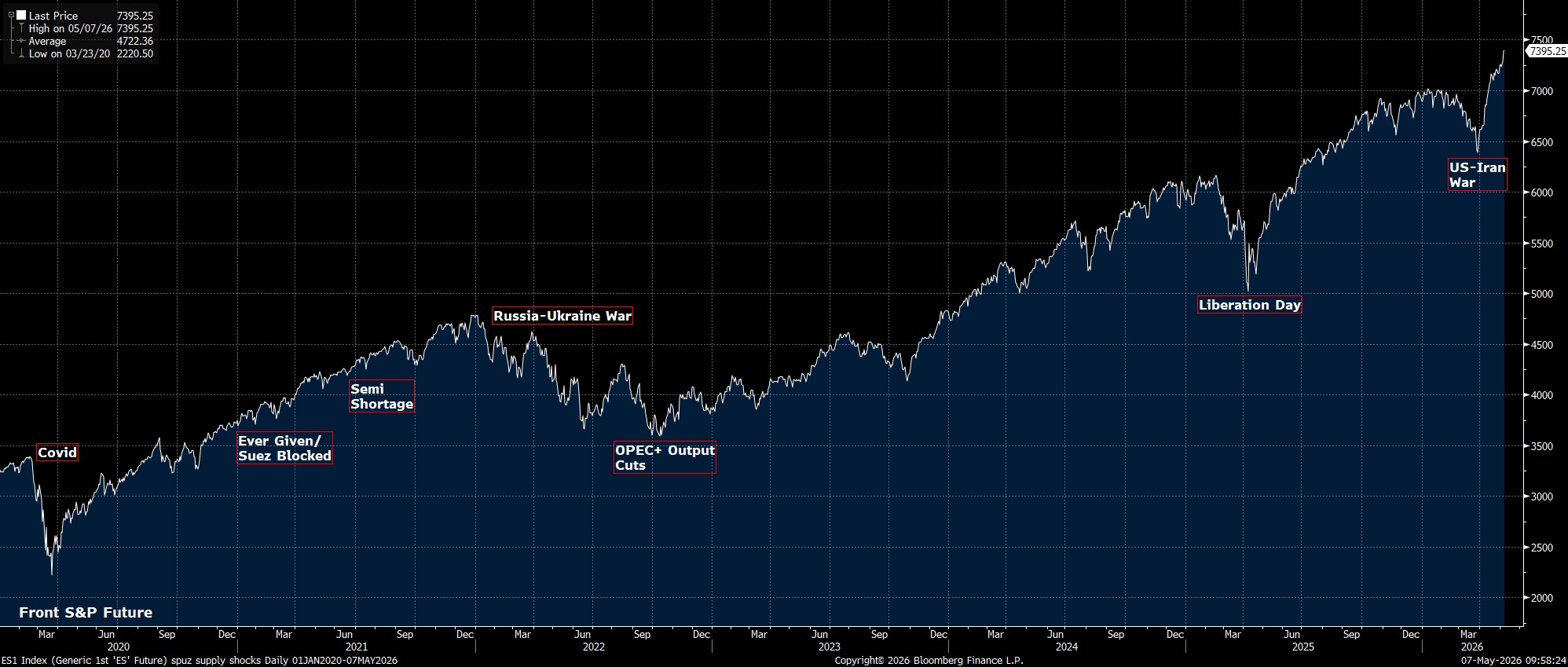

Still, Wall St has certainly not been left out, with record highs being seen across the board, as the tech sector continues to lead the way higher, and with spoos trading north of 7400 for the first time.

While there have been umpteen reports of a deal being ‘close’ since the conflict began at the end of February, it does seem that the US and Iran are now closer than ever to coming to an agreement – not only given the volume of reporting on this front, but also considering public comments from President Trump alluding to the likelihood of a deal being done in as short a period as the next week.

Added to which, and as we’ve seen so often of late, market participants aren’t going to wait around for confirmation of ‘good news’, and instead will seek to ‘front-run’ a positive outcome as much as possible. Furthermore, all of these latest developments again help to underscore a point I’ve been making since the start of last month, that the overall direction of travel on the geopolitical front is one that continues to lead towards de-escalation, and that that in turn continues to underpin risk appetite.

To be clear, the conflict is not over, and it could well prove to be the case that no deal comes to fruition. Still, not only does there seem little-to-no desire on either side to re-escalate in terms of kinetic action, but one should also expect that the path to peace is going to be a bumpy one. As long as we’re on that path, though, stocks should continue to head higher, with dips likely to be not only shallow, but also used as buying opportunities.

The 'Pain Trade' Is Higher Still

On that note, anecdotally, it seems that there are still plenty of market participants out there who are in disbelief at the risk rally we’ve seen, not only this week, but over the last six weeks or so. This suggests, to me, that positioning on the whole is probably still fairly underweight, and that the rally could well still have a long way to run, as those who are still on the sidelines are ultimately forced to buy back in.

We’re back, as a result, to thinking of the powerful FOMO (Fear Of Missing Out) and FOMU (Fear Of Materially Underperforming) forces that have acted as such powerful drivers of upside in the recent past. The ‘pain trade’ is higher.

US Outperformance Is Likely To Return

Of course, risk assets don’t yet appear to have concerned themselves especially much with the economic fallout, in terms of higher inflation and slower growth, that the negative supply shock triggered by the conflict will cause. On this, I’d make two points.

Firstly, while there will undoubtedly be some degree of economic damage to come down the pipeline, even if the Strait of Hormuz fully re-opened this minute, the shock of $100bbl crude is unlikely to be anywhere near as significant as it would’ve been some years ago. DM economies are less energy-dependent, and less manufacturing dominated than they once were, while consumers are not only spending less as a percentage of overall consumption on energy than in years gone by, but are also cushioned to an extent by the positive ‘wealth effect’ that higher asset prices will prompt.

Secondly, that shock will not impact all markets equally. The US, for instance, appears to be in a considerably better position than peers to weather this storm, given its degree of energy independence, as well as considerably more resilient consumer balance sheets. This augurs well for a return to the dynamic of ‘US exceptionalism’.

On that note, the other factors, besides geopolitics, that have propelled the market higher – namely, a return of euphoria around the AI theme, as well as stellar earnings growth – are also areas where the US continues to expel, and Europe continues to lag behind, further supporting the aforementioned theme, that one could simply express in a long SPX/short SXXP position.

_Daily_2026-05-07_09-58-58.jpg)

Muddling Through A Supply Shock Is Nothing New

One final point that I’d make here, is that while recent events in the Middle East have no doubt been significant, and worrying for those in the region, and elsewhere, a negative supply shock isn’t anything new for markets.

In fact, the 2020s thus far have been marked by a series of such shocks, in many forms, all of which have initially sparked a sharp drawdown, but all of which have also seen the market ‘muddle through’, continuing to climb the ‘wall of worry’. None have derailed the broader bullish trend, underlining the incredible resilience of capital markets. This time is unlikely to be any different.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.